PHASE 2: DEFINE

Sketching out a simplified flow

As with all payment-based apps, we had to start first with the perception of security, including the user's sense of control. We wanted to make sure they felt comfortable throughout the process.

Convenience versus the creep factor

We'd been watching the sea change from "I don't want my bank knowing anything about my bills" to "my bank should help me out without my asking them to," and this feature was falling in line with that.

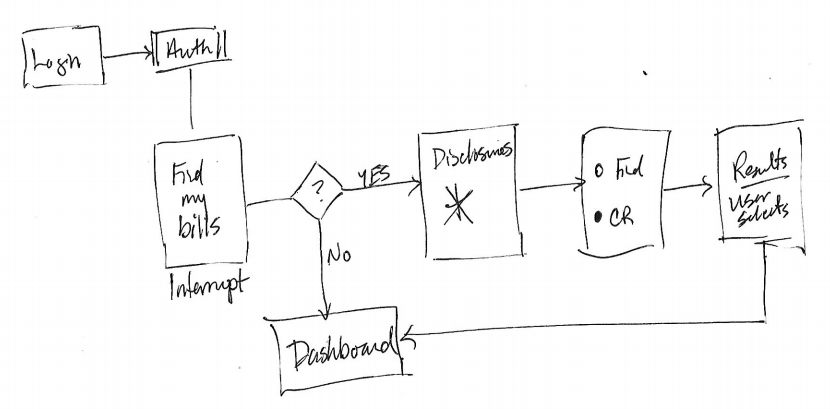

But research had shown that consumers wanted to be in control of the process, so no "auto-discovery" without them kicking things off. This added a couple of steps into the flow, which we roughly sketched out and tested with a bare bones prototype.

Context, context, context

Throughout the research and definition phase, we continually focused on our design intent of honoring the user's current context. We were about to interrupt their day; they might be accessing our app while away from home and, therefore, their paper bills; they might not even get paper bills and not want to flip back and forth between apps.

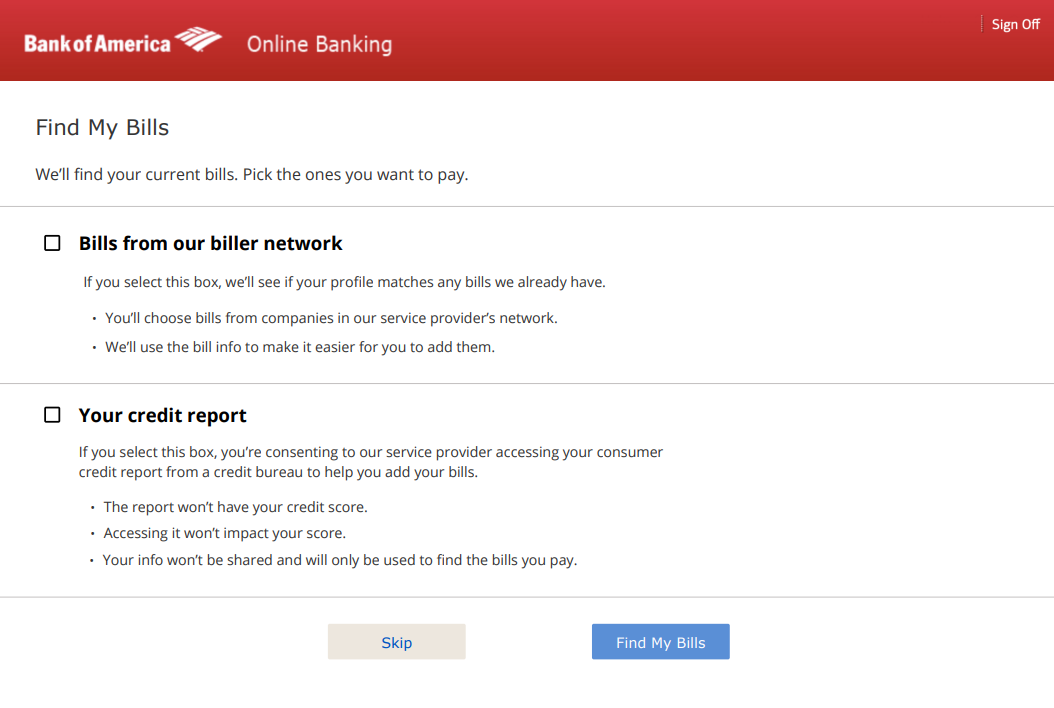

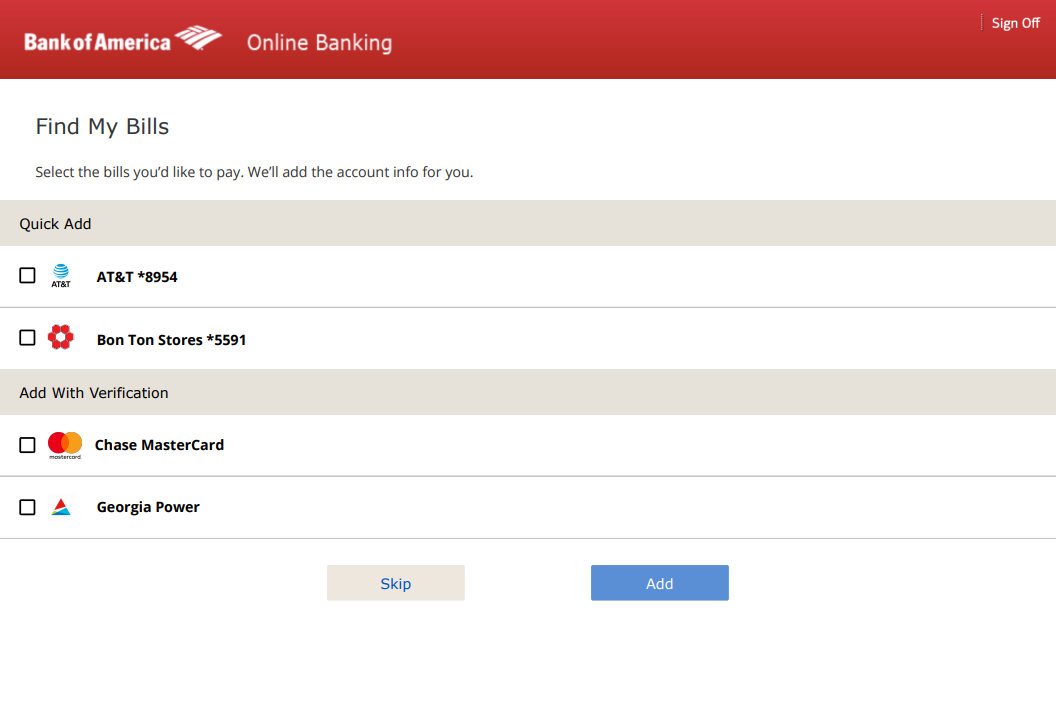

This meant simplifying everything as much as possible: the language, engagement options, and user interactions. We developed some basic guidelines: use bullets instead of a paragraph of text for legal language; show the "easy" options that don't require the user to look up anything first; allow the user to quickly skip past the feature if they wanted to.

Making the hard sell

One feature on offer in this new onboarding flow involved getting a little personal with users and their credit reports. Given the current situation of fraud alerts and identity theft, we knew consumers might not want to use that particular option.

So we focused hard on the messaging to make sure users felt comfortable with that service. During our research, we A/B tested different content presentations and tones. With the results of that testing in hand, we were ready to move into building wireframes.